With lot of discipline and hard work you spent a decade or two saving up for your early retirement. Now how to be sure if you have saved-up enough or not? Safe Withdrawal Rate answers this particular dilemma: How much can you spend in Retirement based on your savings.

Any Retirement planning whether Early or Traditional has two phases: (1) asset accumulation phase followed by (2) post-retirement spending phase. When we started planning for our own early retirement we discovered the FIRE community used a thumb-rule called 25X for accumulation phase and 4% safe withdrawal rate (SWR) for post-retirement spending phase. We also started our FIRE journey with these assumptions, but we now understand these rules and their limitations much better and we will share them with you in this post.

In our earlier blog post How much I need to retire early In India, we shared our views on how much to save to retire early and our opinion on the 25X strategy. In this post we will share our views on the post-retirement spending phase for which the most common thumb rule is the 4% safe withdrawal rate.

FUN ALERT🙂 WE HAVE DONE OUR OWN LITTLE EXPERIMENT BASED ON HISTORIC DATA AVAILABLE IN INDIA TO SEE THE VIABILITY OF 4% RULE. THAT IS ALSO A PART OF THIS BLOG POST!

TABLE OF CONTENT

Challenges with planning the post-retirement spending

It is a complex exercise to plan for post retirement spending because of reasons such as: Inflation, one’s life span, Market volatility, unforeseen expenditures. The longer you plan to live on your retirement corpus the higher is the risk of things going wrong.

This is where Safe Withdrawal Rate (SWR) comes into the picture, since it is a conservative estimate of how much you can safely withdraw annually from your nest egg without exhausting it completely before you die. SWR approach balances between you having enough money every year to live comfortably after retirement without depleting your corpus prematurely.

Is there a universally excepted Safe withdrawal rate that one can use?

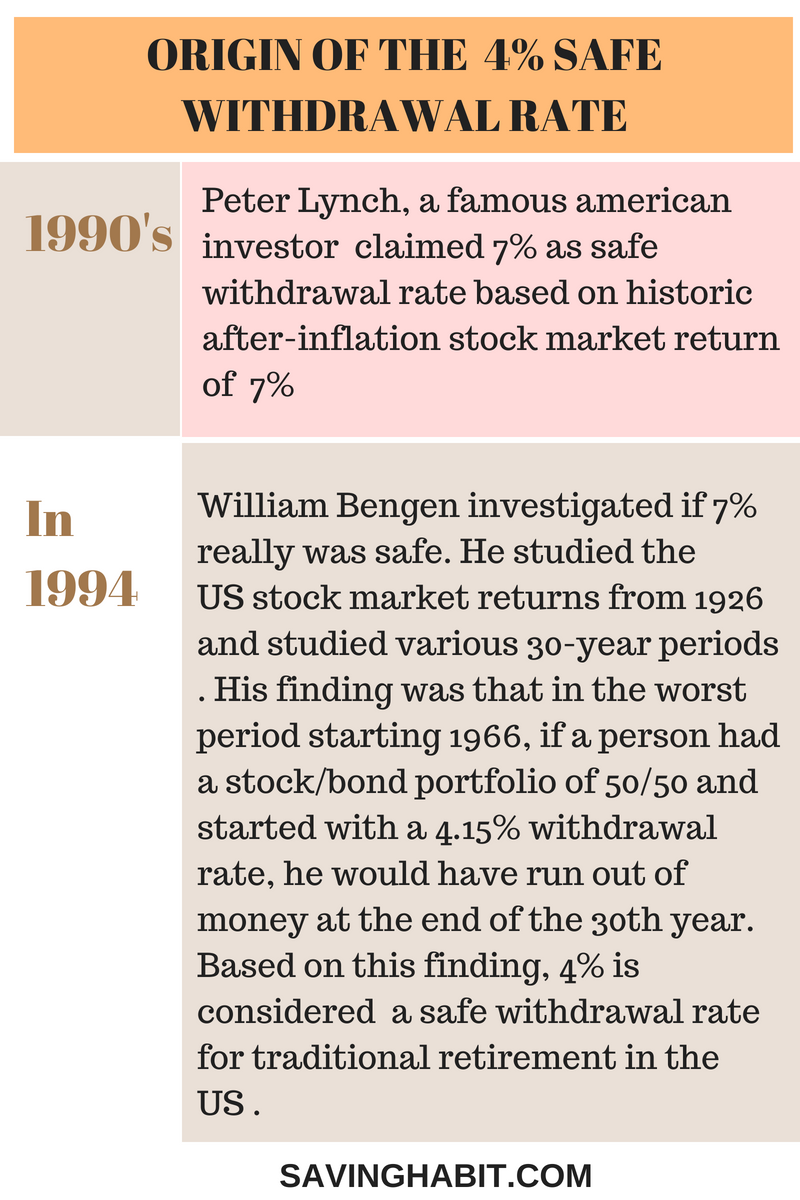

Most of USA literature swears by 4% Safe Withdrawal rate.

Origin of 4% Safe Withdrawal Rate

The 4% safe withdrawal rate is not proven to last forever 100% of the time. and that is what happened to people who retired in year 1966, their money just about lasted for 30 years.

It’s really important to recognize that the word “safe” should be taken with a grain of salt since it’s based upon what’s happened historically. If markets behave differently than they have in the past, what was safe in the past may not be safe in the future.

William Bengen- In an interview

How 4% Safe Withdrawal Rule works

- Assume your annual expenses at the time of retirement is Rs.12 lakh and your retirement corpus is 25X = 3 crore (25 times Rs.12 lakhs)

- As per 4% withdrawal rule, in the first year you will apply 4% withdrawal against your retirement corpus of 3 crore. So in your 1st year, withdrawal would be Rs.12 lakh (4% of Rs.3 crore)

- Second year onwards, forget about 4% and never look at it again. Instead take the previous year’s consumer inflation and add it to the previous year’s withdrawal to calculate your annual withdrawal amount.

- For example: say previous year’s consumer inflation is 8%, you then add 8% of Rs.12lakhs = Rs.96K to the withdrawal. So, the second year withdrawal would be Rs.12lakhs + Rs.96K= Rs.12.96lakh (Rs.12,96,000)

- Each year you simply increase the withdrawal according to the inflation rate so that your lifestyle keeps pace with inflation.

Applying 4% SWR to Indian context

We ran our own little experiment based on William Bengen’s study. We assumed:

- 50/50 stock/debt portfolio

- Person retired in year 1996 with 25X corpus of 3 crore, based on Rs.12 lakhs annual expense.

- Withdrawal Rate is 4% rule in all scenarios

FIRST SCENARIO: Actual returns for first 22 years, Assumed returns after 22 years (1.5% Real Rate Of Return)

- We used actual numbers for equity+debt returns & inflation in India for the past 22 years from 1996-2017. Since data is not yet available beyond year 2017, we assumed static returns for simplicity: Equity returns @ 10%, Debt Return 5%, Inflation @ 6%.

- The reason we’ve used base year 1996 is because the first major revamp of the BSE Sensex happened only in 1996 not to mention various stock trading scams in the early 90s. You can read the timeline with commentary here and here.

- Under these assumptions 3 crore lasted for 40 years.

*Why Real rate of returns?: One of the major factors that affects any investment returns is nothing, but INFLATION. This is invisible, but eat away the real growth of any investment and eventually you may find that the investment has actually grown very less or the growth has been only negative (if inflation is higher than the generated returns). The inflation adjusted returns is called as “Real Rate of Returns”

SECOND SCENARIO: Assumption 2% Real rate of return*

- Under these assumption 3 crore lasted for 34 years.

THIRD SCENARIO: Assumptions 3% Real Rate of Return

- Under these assumption 3 crore lasted for 42 years.

FOURTH SCENARIO Assumption 4% Real Rate of Return.

- Under these assumption 3 crore lasted for 64 years.

The excel sheet has 4 tabs, use arrows buttons at the left bottom of the excel to see all 4 scenarios. You can even download this sheet by clicking download button on bottom right of the excel sheet. YOU CAN CHANGE THE NUMBERS TO TEST YOUR OWN ASSUMPTIONS AFTER DOWNLOADING THIS SHEET

Disclaimer: In the above Excel sheet, we have used actual data for returns & inflation from BSE & RBI only to simulate dynamic returns and not for any other purpose.

Overall we feel more relaxed after running these numbers.

Our conclusion

- We advise readers to be bit conservative rather than being overly optimistic while planning Safe Withdrawal Rate. Also keep revisiting the assumptions every 5 years as more and more data will be available and you will also be closer to the retirement date.

- We highly recommend fellow FIRE enthusiasts to plan for active income after early retirement even if it is part-time work just in case the need arises.

- In our previous blog post How much money I need to Retire Early In India we said that we are targeting 25X as a starting target but will be most comfortable hanging our boots fully when we reach 40X. Regarding Safe withdrawal rate we will monitor how the next decade plays out, but at the moment we are considering anywhere between 2-3% safe withdrawal rate for post retirement withdrawal.

Watch out for

- Bad sequence of returns

- Tax implications on post Retirement withdrawal income

In our future posts we will write about how bad sequence of returns and tax can impact early retirement plans.

Feel free to share this blog post with your friends and family who are interested in FIRE.

NEXT TO READ:

How much money I need to Retire Early In India

The basics of Financial Independence and Retiring Early (F.I.R.E)

Early Retirement in India- Ultimate Guide

Early Retirement Interview: Anil from Pune is 4 years away from Financial Independence