The most difficult question to answer while planning for early retirement is- How much money I need to retire early? We have spent a fair amount of time thinking about the most optimal early retirement corpus number. In the end, we figured out the most straight- forward approach is to equate the retirement corpus to (X) times your annual expense. (X) being the number of years of expenses you want to save.

In this post, we will help you estimate how much money you need to retire early in India. This is a rough guideline that we have used to calculate our own early retirement corpus.

TABLE OF CONTENT

How much money do I need to retire early In India?

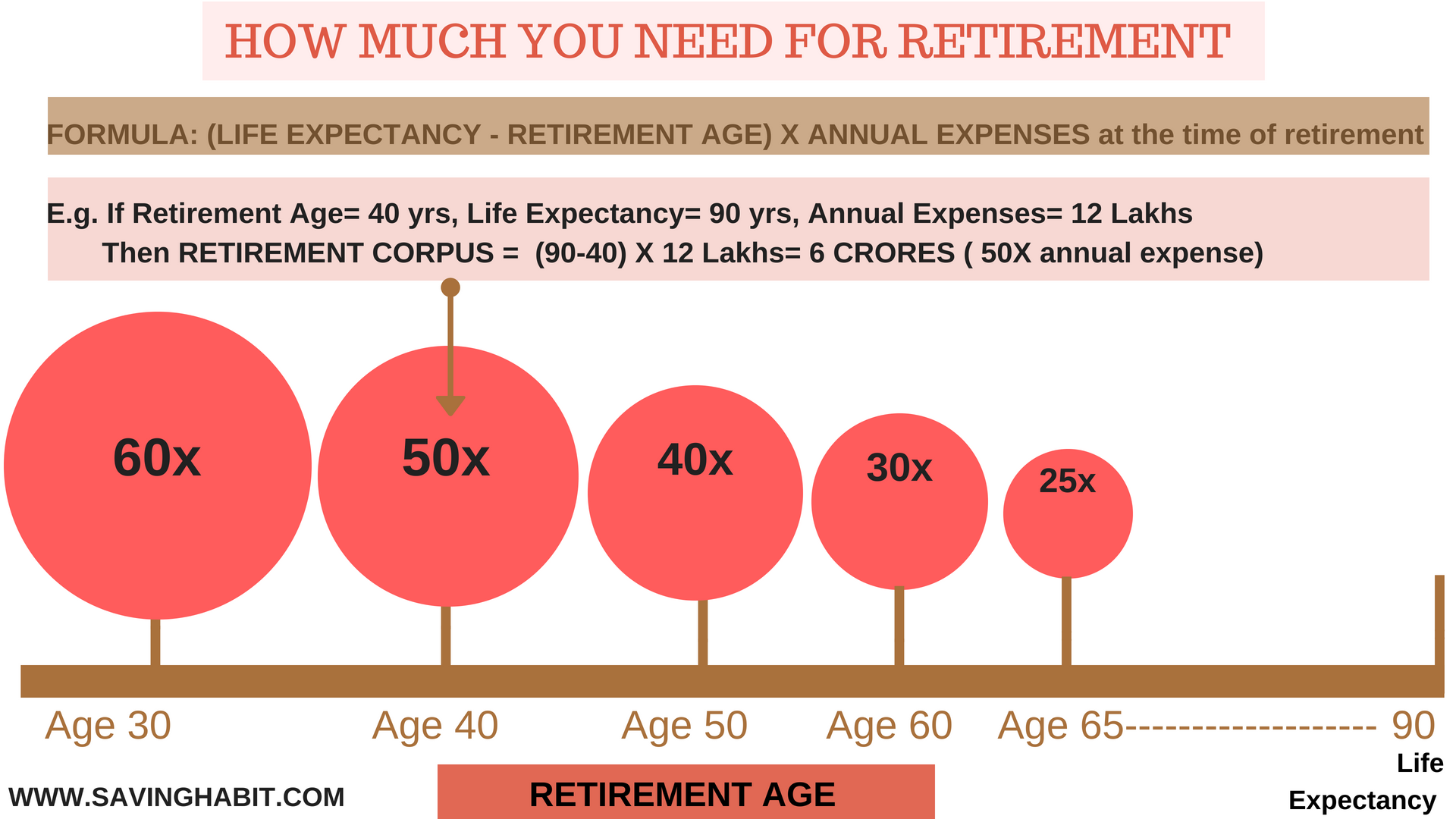

In this approach, the corpus you need is 1. Your INFLATION adjusted annual expenses (MULTIPLIED BY) No: of years of expenses, you want to save.

Step 1: Calculate your Inflation-adjusted annual expenses

Take your current annual expenses and adjust it for inflation depending on when you want to retire early.

For Eg: If you are age 30 and have an annual expense of 12 lakhs, and plan to retire by age 45, assuming an inflation rate of 6% you will need 28 lakhs in future value.

Current Age: 30

Current Annual Expenses: 12 lakhs

Retirement Age: 45: years to retire 45-30= 15 year.

Inflation: 6%

Annual Expense at the time of retirement= 12 lakhs * 6% inflation for 15 years= 28 lakhs per year.

Step 2: Establish how many years worth of expenses you want to save:

This is the most debated subject in the Early retirement community: How many years of expenses must be saved before hanging up your boots?

The conundrum is you save too less, you will exhaust your retirement corpus before you die. To save the fattest corpus possible- you need to work much longer. How to find the right amount to live happily on after you retire?

A blogger named Mr.MoneyMustache (MMM) is a rockstar in the F.I.R.E community for having confidently declared himself retired early at age 30 in the year 2005 to raise their young baby. 13 years later he is about 43 years old now. That is a lifetime in the F.I.R.E community and hence he is a role-model for Early Retirement.

He recommends an early retirement corpus of 25 times your annual expenses at the time of retirement, also referred to as 25X.

What is 25X based on

MMM says:

Take your annual spending, and multiply it by somewhere between 20 and 50. That’s your retirement number. If you use the number 25, you’re implicitly using a 4% Safe Withdrawal Rate, which is my own personal favorite number.

So where does this magic number come from? At the most basic level, you can think of it like this: imagine you have your ‘stash of retirement savings invested in stocks or other assets. They pay dividends and appreciate in price at a total rate of 7% per year, before inflation. Inflation eats 3% on average, leaving you with 4% to spend reliably, forever.

- MMM’s theory of 25X for Early Retirement is based on the Trinity Research Study for traditional retirement spanning a maximum of 30 years.

- Early Retirement enthusiasts claim that if you can live on an above-inflation return of 4% from your 25X retirement portfolio, your corpus will last forever. Share on X

- Not sure if 4% withdrawal rate right for? Read our blog post Safe Withdrawal Rate- How long will your money last in retirement.

It is essential to understand how 4% safe withdrawal works. So we recommend you read the above post.

Our take on the 25X approach

There was once a naive time in the past when we believed this simplistic math because we desperately did not want to work in unhappy jobs ever again.

25X seemed like the shortest target we had to reach. But after coming across the following limitations, we’ve become a bit sceptical about the 25X target. And more conservative in our approach:

- The Trinity Research Study quoted by the F.I.R.E community is a study done for traditional retirement. It shows that a retirement corpus will last for 30 years with a 4% safe withdrawal rate even if there are market downturns. But we are not aware of any such study done for Early Retirement which by definition lasts for more than 30 years throwing a big question mark on whether 25X alone is enough to retire early and live off for say 40-50 years.

- High inflation in India eats up most of the investment returns. Even headline inflation is 6% so our lifestyle inflation must be much higher. Share on X

- Unforeseen old-age healthcare expenses and inflation in health insurance premium.

- Broken public amenities in India require you to spend extra for private backups

As a result of the above reasons, we’ve changed our attitude towards this math, work and early retirement in general. It is better not to have a corpus that is “just enough for living expenses” dependent on unpredictable market returns.

Safest Approach

We now believe that the safest approach is to target a corpus of annual expenses (times) the number of years you expect to live after early retirement. Assuming zero real returns i.e. investment returns just meet the inflation.

Points to consider:

- Sooner you want to retire- more no: of years you will live on your retirement corpus and bigger it needs to be.

- If you are rigid about not wanting to work again then go with the exact number you get after the above calculations.

- But, If you are flexible and willing to do some part-time work to cover some part of your expenses you can quit the job with much less corpus. keep reading to know how.

25X corpus is better suited for a traditional retirement around age 65 because 25 years of expenses work out to a life expectancy of age 90, the age till which most people expect to live. Share on X

Our Practical Approach : 25X Corpus + Active Income

Don’t worry if a corpus of 50X or 6 Crore by age 40 seems like a really large number!

If you are like us and want to use early retirement to make a career shift, start a business or even travel the world we recommend a more practical plan.

This approach balances your desire to live your life at the earliest and the hard truth that you need a safety net before embarking on that life. Here goes:

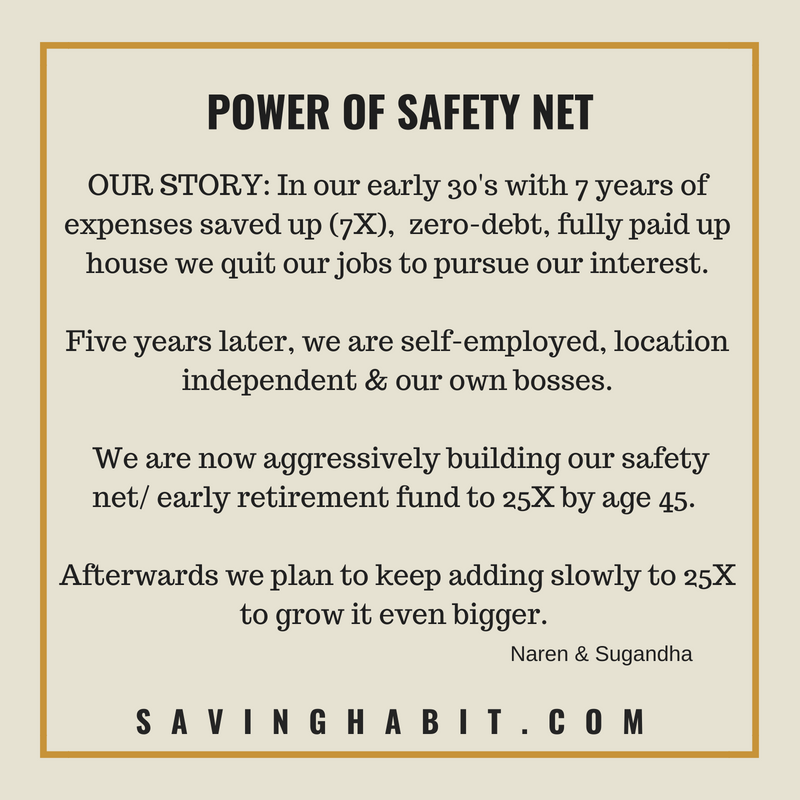

- Age 30-45: Target 25X within 10-15 years to become financially independent first. This is very much achievable with a savings rate of 50%. Start early in your 20s if you can.

- Age 45-50: With 25X of expenses as the safety net, you can afford to quit your job and figure out how to make money from your real interests in life. A new venture can take 3-4 years of focus before it starts covering your living expenses.

- Age 50-65: Once your new venture succeeds, invest any surplus to grow the 25X to give yourself a really secure old-age retirement. You have another 15 years to grow the 25X into say 40-50X.

This approach allows you to pursue your passion early in life using a reasonable safety net of savings.

If the thought of “working” after Early Retirement puts you off, I recommend re-reading the section above on inflation in India that convinced us that working on something we like from a position of strength is better than running out of money and being forced to work from a position of weakness.

So yes! we recommend 25X corpus as the Early Retirement Target. but not to live off of it for the rest of your life. but to use it as a safety net for a few years when you make the leap into the unknown.

%3Abrightness(10)%3Acontrast(5)%3Ano_upscale()%2Fiwruggia0098c-56a066735f9b58eba4b0445e.jpg&imgrefurl=https%3A%2F%2Fwww.thebalance.com%2Foverdraft-line-of-credit-315353&docid=vberPkhOAVhenM&tbnid=AIQOCbv7kNIkpM%3A&vet=10ahUKEwjo4aiJ3JjcAhVEL48KHQPTChUQMwh0KCwwLA..i&w=300&h=200&safe=active&client=safari&bih=678&biw=1439&q=tight%20rope%20walking%20safety%20net&ved=0ahUKEwjo4aiJ3JjcAhVEL48KHQPTChUQMwh0KCwwLA&iact=mrc&uact=8)

A word on Opportunity Cost: 25X vs. 50X

Most F.I.R.E aspirants don’t seem to recognize that their Life is passing them by as they try to build the largest corpus possible before quitting jobs they don’t like.

The downside of trying to save 50X in 10-15 years is that you have to earn a lot of money sacrificing your prime youth in the process. That is the opportunity cost of trying to build a huge “war chest” before taking even the first step towards your dream life.

To put it bluntly: If you don’t feel confident with 25X you may not feel confident even with 50X.

We are grateful to Mr.MoneyMustache for helping us understand that Early Retirement is possible with the help of reasonable savings, can-do attitude and some active income after retirement.

But his passionate followers make the mistake of assuming that his 25X corpus recommendation is the “maximum” corpus needed. When in fact it is the “minimum” needed to balance the opportunity cost of living the life you want versus slogging till age 60.

I’m quoting his exact words below to explain this better (I’ve bolded the most important sentence) :

… you don’t have to be insanely conservative, working for year after year to ensure a gigantic starting nest egg before daring to retire.

…Once you quit a full-time job, you just need a small positive savings rate to stick around and keep trickling into investments. This will automatically become a cash snowball as you go about your daily retired life. By the time you’re old enough to need it, it will be bigger than you can possibly need.

We hope this post helped you to come up with your own early retirement corpus target that works best for your lifestyle and future plans.

Please feel free to ask us your questions in comments.

Also, we would love to hear in comments what is your early retirement corpus target and why.

ENJOYED READING THIS BLOG POST?

Subscribe by E-mail for more awesome information on Early retirement. We publish one new post every week!!! It is Free!

Recommended Reading:

Safe Withdrawal Rate- How long will your money last in retirement

Sequence Risk Impact on Early Retirement

Tips For Starting A Business After Early Retirement

Show your love on social media:

If you like our blog posts! please do LIKE and SHARE it on facebook, twitter or Whatsapp!