Even before our Son was born, Naren and I discussed in detail whether or not we should pay for our kid’s college. We both decided that our Son should be able to at-least graduate from college debt-free so he is free to pursue career & life choices.

An opportunity presented itself when our parents gave us some cash for our pre-pregnancy expenses. Since we had already kept a pregnancy fund aside when we got married, this was extra cash for us. We were tempted to use the gift money on a baby-moon vacation but we managed to keep our temptation in check, reminding ourselves of Long-term gratification vs. Instant gratification (this deserves a post in itself). That is how we started his college fund three months before his birth.

Education Inflation is double the consumer inflation In India

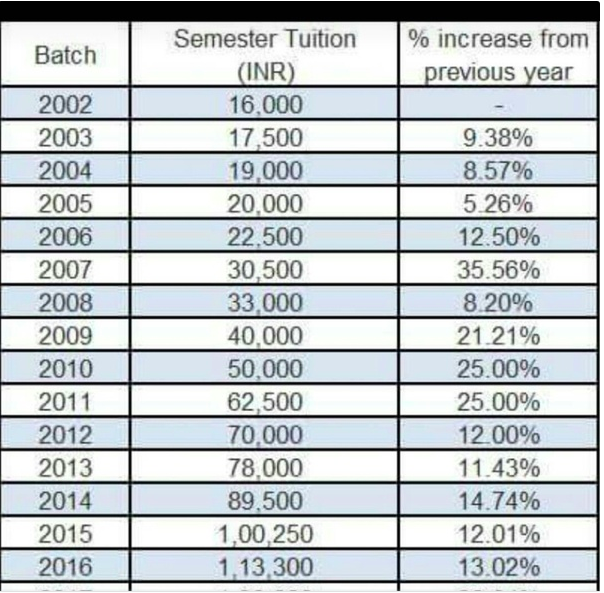

We had some idea that education and healthcare inflation is in double digit % in India. But we were bit shocked to see that the education inflation is roughly estimated at 10-12% in India with no indication of going down in the future. To get a real idea we took BITS Pilani as a benchmark and went through their fees increase from year 2002-2016.

Snapshot of Bits Pilani Semester tuition from Year 2002-2016

- In 15 years the semester cost increased from 16 thousand to over Rs.1 lakh.

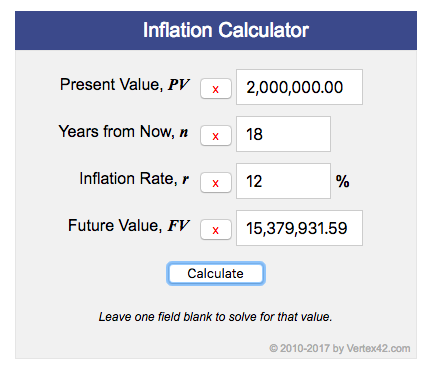

Now how does it translate into future?

Lets us take an example, the current cost of a 4 year course at BITS is approx. Rs.20 lakhs. Estimating future annual education inflation at 12% for next 18 years, the same course will cost whopping 1.53 Crores.

Link to the inflation calculator used. Oh boy we are so glad that we did start early!

Our Kid’s College Fund Target- 1.5 cr in Year 2036

We only plan to fund our Son’s Bachelors Degree in India at this point. In line with above example we are targeting 1.5 crore by the time our son is 18 years i.e year 2036.

- We are only saving for a 4-year college course of any discipline except Medicine which already costs a couple of crores currently if you don’t get into a government college.

- We are using BITS Pilani as a benchmark for a private 4-year college as the fee is increased year-over-year regularly instead of sudden & unpredictable hikes like in the case of IITs. So from a pure planning standpoint, it is a useful benchmark.

- If this education corpus is not enough then our kid can take up a partial education loan for the difference. This is better than being fully in the hole. Like we mentioned in our original Early Retirement Article, we want to balance both our retirement & our kid’s education goals.

Our Strategy to save for Kid’s college fund

It is straightforward – Start building corpus with a long-term wealth creation asset- Equity mutual fund. Closer to the Goal secure the corpus by moving funds to less risky debt instruments.

Debt instruments alone like PPF, Fixed deposits, debt MF’s and even real estate (unless it is land), gold are safe but not good enough to plan for Kids Education because returns are way lower than the 10-12% education inflation.

So we plan to invest in Equities through Mutual funds:

- We will aggressively invest in Equity Mutual Funds for the first 14 years. However around midway when our Son is 7 years we will start to book profit from Equity. Market permitting we want to maintain 30% of total investment in debt instruments by the time our son is 14.

- To ensure the availability of fund closer to the goal, we will start Systematic Transfer of the remaining college fund from Equity to debt 4 years prior to the goal date.

Below math is bit crude, but we wanted to start right-away instead of waiting till we had every investment detail listed meticulously.

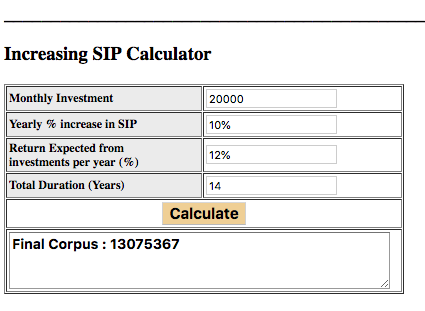

- We used an online SIP Calculator to compute the Monthly Mutual Fund SIP for first 14 years:

@ Rs.20K SIP with a 10% increase y-o-y for the next 14 years will give us 1.3 crore pre-tax.

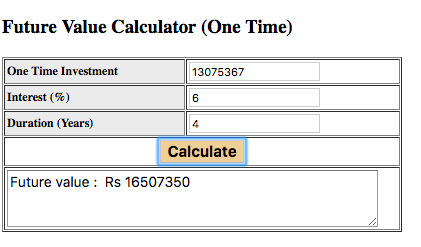

- Then crudely we used lumpsum calculator to see if we moved this money 4 years prior to goal into FD @ 6% return how much will it be:

Of-course we have to still fine-tune for taxes, and select debt instruments-it may or may not be FD. But we think in real life it is better to start investing with rough target and then fine-tune it as you go along.

Where do we stand with our Goal?

We started SIP in Mutual Funds 3 months before our Son was born. We are investing in one Large-Cap and one Small-Cap mutual fund.

5% of college fund will be in Gold, since we received it again as a gift from grandparents who had been saving up for this occasion for a while 🙂 There’s some built-in asset allocation already as a result 😉

We started the SIP 3 months before our baby’s birth. This helped us reduce our anxiety about being new parents. It also made us feel confident about ourselves as parents. Also, now that we have our priorities straight we are not tempted to buy that extra cute little outfit with matching shoes for our little baby who will soon outgrow it.

Our Recommendation to fellow Parents

it is not easy to juggle and save for multiple big goals. But keeping focus on achieving Early Retirement helps us to prioritise what is most important. We also recommend the same to our blog readers. Identify the goals most crucial to you and start investing early towards those goals so that compounding can work for you.

Same would be more clear from this example: We took 3 different scenarios of saving up before kid turns 18 and building on the previous example of college fund target of 1.5 crore, through SIP in Equity Mutual Funds. Return and inflation fixed at 12 %. See the target SIP to reach the Goal:

-

If you start SIP 3 yrs before birth – Rs. 10,581 per month

-

If you start SIP at birth – Rs. 12,034 per month

-

If you start 5 years after birth – Rs. 20,216 per month

Please share with us in comments your plans to fund your child’s college education and any scenario we might have missed!

ENJOYED READING THIS BLOG POST ?

Subscribe by E-mail for more awesome information on Early retirement, personal finance and our life in Goa!!. We publish one new post every week!!! Its Free!

Show your love on social media:

If you like our blog posts! please do LIKE and SHARE it on facebook, twitter or whatsapp!